The meaning of "bequest" isn't straightforward, obvious, or intuitive, even for lawyers. Many assume they know the meaning of the term and overlook its complexity. A close reading of the definition of "bequest" in Black's Law Dictionary is important because this dictionary is considered authoritative by many courts and even the Internal Revenue Service.

Here is the definition of bequest from Black's Law Dictionary (11th ed. 2019):

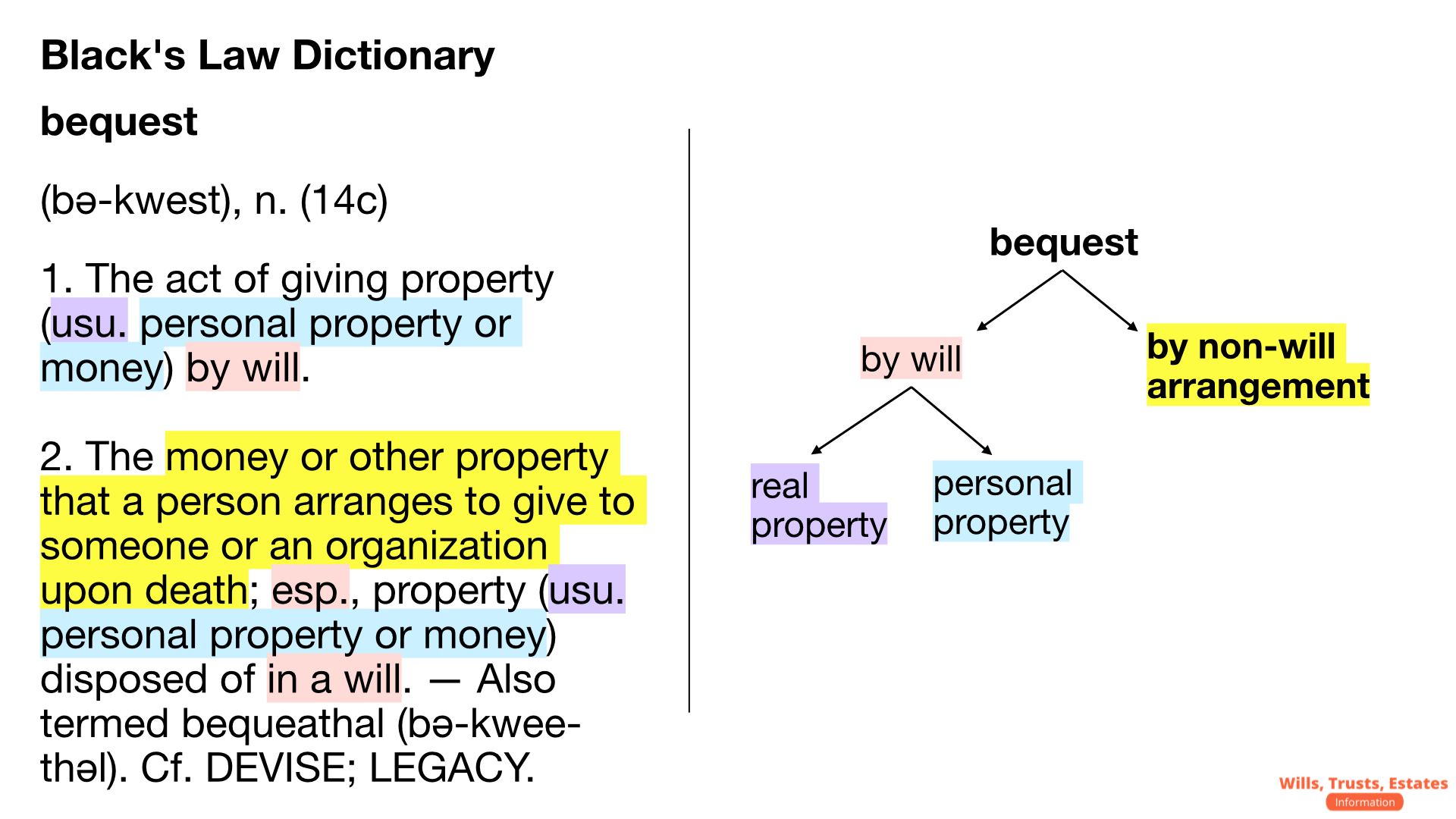

bequest

(bə-kwest), n. (14c)

- The act of giving property (usu. personal property or money) by will.

- The money or other property that a person arranges to give to someone or an organization upon death; esp., property (usu. personal property or money) disposed of in a will. — Also termed bequeathal (bə-kwee-thəl). Cf. DEVISE; LEGACY.

There are two definitions for the term "bequest" in Black's Law Dictionary. The first is a narrow definition of property passing "by will." The second is a broad definition of any arrangement to give to someone or an organization money or other property upon death.

According to Black's Law Dictionary, a "bequest" means many things:

- broad definition: a transfer of property by any arrangement at death

- narrow definition: a transfer of any property by will

- usual meaning: a transfer of personal property by will

- alternate meaning: a transfer of real property by will

It is easy to miss these disparate meanings, so I color-coded them in the graphic below, and I organized them visually in a chart:

Most people overlook or ignore the second, broader definition of "bequest" in Black's Law Dictionary, as the IRS did in Revenue Ruling 2023-2. It is uncontroversial to conclude that confining the term to its narrow meaning can lead to its misapplication.

The meaning of the term "bequest" is crucial to the interpretation and application of Internal Revenue Code section § 1014(b)(1), which states that "[p]roperty acquired by bequest, devise, or inheritance, or by the decedent’s estate from the decedent" gets its basis adjusted to the fair market value at the date of the decedent’s death (emphasis added).

In Rev. Rul. 2023-2, the IRS concludes that assets in an irrevocable trust do not get a basis adjustment under IRC § 1014 on the death of the owner of the trust for purposes of the income tax when the trust's assets are not included in the grantor's gross estate for purposes of the federal estate tax, the liabilities of the trust do not exceed the basis of the assets in the trust, and neither the grantor nor the trust held a note on which the other was the obligor.

The IRS justifies its conclusion by showing that the property does not fall "within one of the seven types of property listed in § 1014(b)."

But the IRS only quotes the narrow definition of "bequest" from Black's Law Dictionary. Nowhere in Rev. Rul. 2023-2 does the IRS mention or discuss the broad definition of "bequest" in Black's Law Dictionary. By saying nothing about the second definition, the IRS leaves room for taxpayers to rely on it.

In a surprising twist, taxpayers do not have to argue that the IRS got it wrong in Rev. Rul. 2023-2. They can concede the IRS's conclusion in the ruling. The trust is not a will, so it is not a "bequest" in the narrow meaning of the term and the property in the trust is not part of the decedent's probate estate.

But by applying the second, broader definition of "bequest" in Black's Law Dictionary – the very dictionary the IRS relies on – taxpayers can reach a different conclusion than the IRS.

The second definition in Black's Law Dictionary leads to the unexpected conclusion that assets in an irrevocable grantor trust qualify for a basis adjustment on the death of the grantor because the property is acquired by "bequest" under IRC § 1014(b)(1) and, therefore, the property is acquired from or passed from the decedent to the beneficiary for purposes of IRC § 1014(a). Such trust assets are, by definition, a "bequest" because they are "money or other property that a person arranges to give to someone or an organization upon death."

⚠️ Please note: Per the disclaimer, this discussion is not legal or any other kind of advice. It is information only for purposes of discussion. • Also, I am in no way suggesting that taxpayers should take a different position than the IRS. I am merely pointing out that a close reading of the definitions of "bequest" in Black's Law Dictionary leads to a surprisingly different conclusion than the one the IRS reached. • For taxpayers who want to take a position against the ruling, Alan Gassman has this suggestion: "Although there is the risk of penalty, a taxpayer might consider paying the capital gains tax on the tax return as if the assets did not receive an adjustment in basis, and then filing an amended tax return requesting a refund based on the assets receiving a step-up in basis, and providing full disclosure that this position was taken. Then, if the step-up in basis is denied, the taxpayer did not make a substantial underpayment on the original return, and the risk of penalties being incurred by the taxpayer should be greatly reduced."

{kind=link}

Leave a Comment